Written By Investec Wealth & Investment Limited

As we start a second week of lockdown and the uncertainty continues around the US Election and Brexit, we thought it would be useful to give you an update on the current macroeconomic and investment climate.

Our aim is to cover a number of areas – general update on market performance year to date, the current coronavirus situation, the US Elections updates, the positive impacts of fiscal and monetary stimulus and a look at where to invest.

Looking back at the market since the beginning of 2020, we can see that UK equities have been one of the worst performing equities markets over the period down 19.5%. By contrast, overseas equities have performed much better. The FTSE World index is up +6.7% since the start of 2020. In several European countries’ bond yields are negative across many maturities, with German 10-year Bonds yielding -0.64%. The situation in the UK is barely brighter, with the 10-year Gilt currently offering a yield-to-maturity of 0.22%. Given that 10-year inflation expectations in the UK are for an average of 3.1%, a loss of value in real terms is guaranteed if held for the full duration – assuming, of course, that the market’s ability to forecast inflation is vaguely correct.

Recently the burden of disease has shifted from emerging markets to the developed markets of the Northern Hemisphere. The total number of global infections are continuing to rise, as a much anticipated ‘second wave’ takes hold. The 7-day average for the past week shows global cases at around 480,000 per day, up 13% week on week. The global death rate has also risen to around 6500 a week but is still below April highs of 7500, suggesting mortality rates have reduced. We are also seeing hospitalisations begin to increase as ICU’s beginning to fill up. But thankfully not at the same rate as the first wave. Many believe that new treatments and greater knowledge of the virus are the key reasons for this.

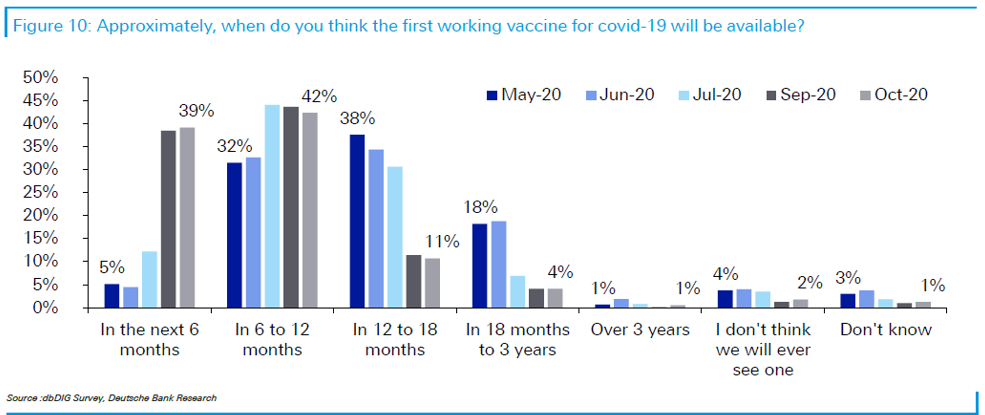

The goods new though is that, although another lockdown will inevitably slow recovery, it is anticipated that the hit to the economy from this lockdown will be substantially less than in April. In addition, the prospects of a vaccine being found remain strong, progress is continuing at a rapid pace, with many vaccines recently entering phase 3 trials. Recent survey predicts vaccine within 12 months.

As the US election unfolds, markets have responded well to the notion of a Biden victory, as it increases the likelihood of a sizeable fiscal stimulus being injected into the US economy quickly. However, future tax rates for corporations and wealthy households are likely to increase under Biden. But a potential Republican majority in the house may soften these increases. A Biden presidency would also see a benefit to ESG investments, with Biden set to re- enter the Paris Climate Agreement, potentially re-join the 2015 Iran Nuclear deal and push for an extension of Barack Obama’s affordable care act.

Despite the devastating effects seen globally by coronavirus, governments around the world have decided to put in place fiscal and monetary stimuluses to contain the economic fallout and help countries recover. In the US, 12.3% of GDP has been spent on fiscal stimulus, part of which involved giving out up to $1,200 to many Americans. In fact, studies have found that most people are better off financially under COVID then they were before. In Europe, large programs of loan guarantees have been introduced for businesses. Most recently in the UK, the BoE has announced a further £100bn of Quantitative Easing, which will allow further supportive measures to be put into place by the Chancellor through this second lockdown.

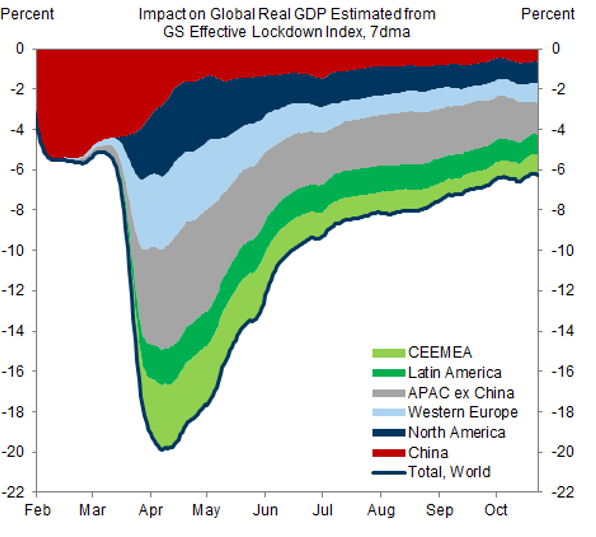

These policies have worked, and countries did initially experience a V-shaped recovery, with GDP Q3 growth rates consistently coming out above the consensus globally. Equity markets also recovered remarkably, recovering from March lows to levels close to those before the pandemic, with the US and Asia above.

As interest rates and bond yields are set to remain low for the coming few years, investors have a decision to make! Stay in cash or similar low volatility investments where the is a high chance of capital been eroded against inflation. Investors are left with the decision on whether to move up the risk scale in order to achieve a return above inflation. In order to make this return, global equities continue to look the most attractive asset class for long term investors. Particularly with loose fiscal and monetary policy likely to continue. Infrastructure and renewable energy are good examples of assets that many believe may offer good opportunities for long term returns. Infrastructure projects, such as the building of toll roads, car parks, hospitals and social housing not only provide income, but also stimulate growth in the economy by creating employment and generating tax income.

To put it succinctly, although we are going through periods of uncertainty, the good news is that governments across the world have responded by ending austerity policies which has led to the V-shaped economic recovery to date. Our base case scenario is still that recovery will be more of a U than a V shaped recovery, it may be a while before growth gets back to pre-covid levels. Currently the US is not expected to see growth until the first quarter of 2022, with the UK only expected to see growth in 2023.